The Law of the Republic of Azerbaijan on the Execution of the State Budget of the Republic of Azerbaijan for 2020 was adopted by Milli Majlis on June 8, 2021. According to this law[1], the state budget revenues in 2020 amounted to 24,681.7 million AZN ($ 14,518.6 million), state budget expenditures amounted to 27,492.2 million AZN ($ 16,171.9 million). 16,656.9 million AZN or 63.1% of the state budget expenditures for 2020 were spent on current expenditures, 8,033.2 million AZN or 30.4% on capital expenditures, 1,726.2 million AZN or 6.5% on servicing public debt and liabilities. The largest share in the implementation of the functional classification of state budget expenditures in 2020 belonged to the sections "Economic activity" (21.0%), "Defense and national security" (14.2%), "General public services" (13.4%), "Social protection and social security" (11.8%), and "Education" (10.5%).

In this article, we will try to identify the corruption risks in the state budget of Azerbaijan and show ways to overcome them. To substantiate our claims, we will refer to the Law of the Republic of Azerbaijan on the Execution of the State Budget of the Republic of Azerbaijan for 2020 (hereinafter the Law), the Draft Law of the Republic of Azerbaijan on the Execution of the State Budget of the Republic of Azerbaijan for 2020, and the Opinion[2] of the Chamber of Accounts on the Annual Report on the Execution of the State Budget for 2020 (hereinafter the Opinion of the Chamber of Accounts).

Risk 1: Budget funds are transferred directly to the executor without a tender.

According to Article 16.1 of the Law on Public Procurement, public procurement of goods (works and services) in the Republic of Azerbaijan shall be carried out by open tender, two-stage tender, limited participation and closed tender, request for proposals, request for quotation, and single-source procurement methods, depending on the conditions of application specified in Articles 17-21 of this Law. In the case provided for in Article 50-1 of this Law, public procurement shall be carried out through e-procurement by using the open tender method.

According to the amendment[3] made to the Decree[4] of the President of the Republic of Azerbaijan on the Application of the Law of the Republic of Azerbaijan on Public Procurement on December 28, 2018, control over the application of the Law is carried out by the State Service for Antimonopoly and Consumer Market Control.

According to the information provided to the Chamber of Accounts by the State Service[5] for Antimonopoly and Consumer Market Control, in 2020, procurement contracts worth 6,567.2 million AZN were concluded with a total of 9,203 procurements in the country by using the methods established by the Law of the Republic of Azerbaijan on Public Procurement. This is 847.2 million AZN or 14.8 percent more in the amount involved in the procurement compared to 2019 and is 2,254 or 19.7 percent less in number.

Analysis of the data submitted to the Chamber of Accounts shows that 3,500.5 million AZN was used for 7,776 competitive procurements held in 2020, which is 1,882 purchases (19.49 percent) less in the number compared to the previous year and 831.6 million AZN (31.15 percent) more in the amount. In terms of numbers, in 2020, the request for quotation was 56.08 percent, the open tender was 26.23 percent, the request for proposals was 2.18 percent, the single-source procurement method was 15.5 percent. In terms of amount, the open tender had a share of 32.8% in the total amount, the request for proposals 18.82%, the request for quotation 1.7%, the single-source procurement method 46.7%.

In general, the dynamics of open tenders over the past 3 years amounted to 2,698 purchases worth 2,266.4 million AZN in 2018, 2,917 purchases worth 2,156.5 million AZN in 2019, and 2,414 purchases worth 2,152.9 million AZN in 2020. As can be seen, while the dynamics of open tender procurement has been declining, the dynamics of non-competitive request for proposals has been increasing over the past three years. Such that it has increased from 237 purchases worth 176.0 million AZN in 2018 to 418 purchases worth 371.5 million AZN in 2019 and to 201 purchases worth 1,236.1 million AZN in 2020. The dynamics show that while in 2020, compared to 2018, the amount of purchases made by open tender method decreased to 113.5 million AZN and the number decreased to 284, in the same period, the number of purchases made by non-competitive, single-source procurement methods increased by 1,060.1 million AZN.

Thus, although the amount of funds involved in public procurement increased in the reporting year compared to the previous year, the number of contracts decreased. As in the previous year, the request for quotations was significant in terms of numbers. In terms of amount, the single-source procurement method was not preferred; on the contrary, there was a decrease in 2020, compared to previous years, in the purchases made by single-source procurement methods, which fully reflects the competitive environment.

However, according to the Law[6] of the Republic of Azerbaijan on Public Procurement, public procurement refers to the purchase of goods (works and services) in the Republic of Azerbaijan by state enterprises and organizations (departments), enterprises and organizations with a state share of 30% or more in the authorized fund at the expense of state funds, loans and grants received and guaranteed by the state. According to Paragraph 2 of the Decree[7] of the President of the Republic of Azerbaijan No. 668 of January 29, 2002, on the Application of the Law of the Republic of Azerbaijan on Public Procurement, all public procurements in the amount of 50,000 AZN and above are carried out through tenders. According to the Decision No. Q-12 of the Board of the Ministry of Finance of the Republic of Azerbaijan dated May 20, 2013, on determining the amount for publication of minimum amounts for public procurement of goods (works and services) by means of open tenders and request for quotations and notification of purchased services in the international media and on the Internet, the minimum estimated cost of goods (works and services) for public procurement by the open tender method was set at 50,000 AZN, the minimum estimated price of goods (works and services) for public procurement by the request for quotation was set at 5,000 AZN. According to the amendments made to the Law on Public Procurement in 2018, the procurement of goods (works, services) with the estimated cost of the subject of purchase in the equivalent of $ 3 million or less shall be carried out only through e-procurement with the participation of micro, small, and medium enterprises by using the open tender method. It is planned to conduct the tender through e-procurement. For this reason, a "single electronic portal of public procurement" has been created.

According to Article 50-1.1 of the Law, the procurement of goods (works, services) with the estimated cost of the subject of purchase in the equivalent of $ 3.0 million or less is carried out only through e-procurement with the participation of micro, small, and medium enterprises by using the open tender method. The e-procurement method using the open tender method is one of the important measures to reduce the corruption risks and prevent abuses in public procurement. However, Article 50-1.3 of the Law allows the procuring entity to avoid open tendering and e-procurement in the above case. It is determined that if the tender cannot be conducted using the open tender method and (or) through e-procurement, a decision must be made by the procuring entity, stating the reasons and conditions justifying it. Since the law does not specify the circumstances and conditions under which open tender method and e-procurement are not possible, it creates conditions for abuse by giving the procuring entity broad discretionary powers. Article 50-1.4 of the Law also creates conditions to avoid the open tender method and e-procurement. According to this article, the open tender method and e-procurement shall not be applied to procurements where the amount of the procurement contract is less than the minimum amount determined by the body (institution) determined by the relevant executive authority. The minimum amount that excludes the use of the open tender method and e-procurement is not defined by applicable law.[8]

Therefore, the Law on Public Procurement should be amended to completely limit the possibility of evading e-procurement. Furthermore, information on non-competitive, single-source procurement methods from the state budget should be regularly disclosed and published periodically. If the standards of transparency and accountability are not met in this regard, the corruption risks of the funds spent by the state budget, mainly on the "Economic activity" section, will remain high. This will ultimately increase the inefficiency of the use of state budget funds.

Risk 2: Budget funds are disproportionate, mostly spent at the end of the year.

According to the Opinion of the Chamber of Accounts, the analysis of quarterly and monthly execution of expenditures by functional classification sections of the state budget last year shows that the highest amounts of execution were recorded in 6 out of 12 sections in the IV quarter and in 7 in December. Even in the IV quarter, including in December, the amount of expenditures on the "Environmental Protection" section was at the highest level, amounting to 43.8 percent and 27 percent, respectively, of the amount executed for the year.

Execution of state budget revenues and expenditures shows that in 2020, 48.7 percent and 44 percent of total budget revenues and expenditures, respectively, were executed in the first half of the year, and 51.3 percent and 55.6 percent in the second half of the year. Based on the monthly reports on the execution of state budget revenues and expenditures by months, the analysis shows that while revenues exceeded expenditures in January, March, October, and November, the opposite trend was observed in other months. During this period, the highest figure, where the execution exceeded the forecast, was recorded as 1,223.3 million AZN in December. Such that although the figure determined by the distribution of state budget expenditures by quarters and months for December was 11.0 percent, the actual figure was 15.5 percent, which is 4.5 percentage points more than the approved distribution.

In general, 29.4 percent of expenditures in 2020 fell to the last quarter of the year. 54.7 percent of this amount was spent in December. For comparison, in 2019, 31.7 percent of expenditures fell to the share of the last quarter, as well as 55 percent to the share of December.

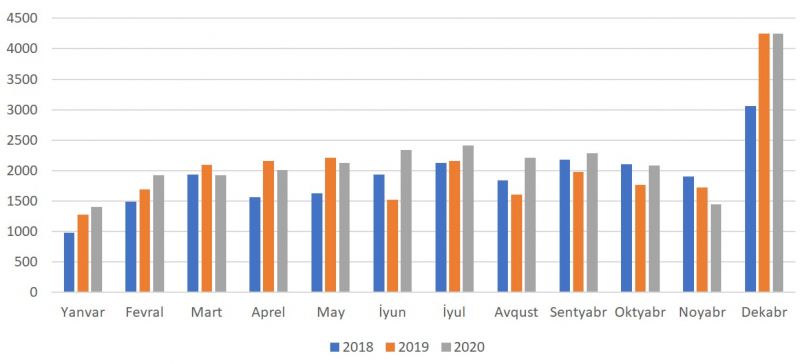

Based on the figures of the last 3 years, the dynamics of the execution of budget by months can be found in the data in Table 1.

| Months | Expenditures of the state budget, in million AZN | ||

| 2018 | 2019 | 2020 | |

| January | 976.5 | 1,276.7 | 1,403.2 |

| February | 1,493.1 | 1,693.1 | 1,927.0 |

| March | 1,938.4 | 2,089.3 | 1,924.4 |

| April | 1,557.9 | 2,161.4 | 2,013.0 |

| May | 1,628.4 | 2,205.6 | 2,124.7 |

| June | 1,929.9 | 1,524.9 | 2,338.5 |

| July | 2,125.0 | 2,151.7 | 2,411.8 |

| August | 1,836.4 | 1,609.4 | 2,213.3 |

| September | 2,180.4 | 1,978.5 | 2,286.3 |

| October | 2,103.9 | 1,766.2 | 2,079.9 |

| November | 1,900.2 | 1,718.5 | 1,440.7 |

| December | 3,061.5 | 4,250.6 | 4,253.6 |

Source: Chamber of Accounts

The state of execution of the state budget for the last 3 years by months can be seen more clearly in the figure below.

Figure 1. The dynamics of the execution of budget by months in 2018-2020, mln.manats

The chart was compiled by the Chamber of Accounts on the basis of reports and figures submitted on the execution of the state budget.

The analysis of the data shows that in December, despite the fact that the average monthly budget expenditures for the first 11 months of 2020 amounted to 2,014.8 million AZN, expenditures in December were 2.1 times higher than the corresponding figure. Such that the funds spent in December amounted to 16.1 percent of total budget expenditures last year (17.4 percent in 2019).

As for 2019, The highest figure, where the execution exceeded the forecast, for this year was observed in December, with 1,590.5 million AZN or 6.3 percentage points. It should be noted that the relevant figure in December 2018 was 641.5 million AZN or 2.8 percentage points. The highest figure, where the forecast exceeded the execution, was observed in November, with 636.7 million AZN or 2.5 percentage points (In 2018, the relevant figure was observed in April, with 407.9 million AZN or 1.8 percentage points).

In 2019, there were differences between the approved figures for expenditures by months and the actual amounts of execution, and the largest difference in both relative and absolute figures was in December. In January, April, May, and December, the execution figures for expenditures exceeded the forecast figures in the reporting year, and the opposite trend was observed in other months.

In the reporting year, as in previous years, the share of funds executed in the IV quarter was higher, and expenditures were mostly executed in December. 31.7 percent of expenditures in 2019 (31.1 percent in 2018) were executed in the last quarter of the year. 55.0 percent of this amount (43.3 percent in 2018) fell to the share of December. Such that the funds spent in December amounted to 17.4 percent of total budget expenditures last year (13.4 percent in 2018).

In the second half of the 2019 reporting year, the executed amounts of the state budget were relatively higher than in the first half of the year. Although revenues exceeded expenditures in 5 months, the opposite trend was observed in the other 7 months. In 2019, 43 percent and 44.8 percent, respectively, of total budget revenues and expenditures were executed in the first half of the year, and 57 percent and 55.2 percent in the second half of the year. According to the analysis of monthly reports on the execution of state budget revenues and expenditures by months, while revenues exceeded expenditures in January, August, September, October, and November, the opposite trend was observed in other months.[9]

In 2018, the highest figure, where the execution exceeded the forecast, was observed in December (649.9 million AZN or 2.8 percentage points), and the highest figure, where the forecast exceeded the execution was observed in April (407.9 million AZN and 1.8 percentage points). As in previous and subsequent years, in 2018, the share of funds executed in the last quarter was high, and both revenues and expenditures were higher in December than in other months. In the reporting year, 43.8 percent and 41.9 percent, respectively, of total budget revenues and expenditures were executed in the first half of the year, 56.2 percent and 58.1 percent in the second half of the year, as well as 31.1 percent of total expenditures for the year (27.3 percent in 2017) in the last quarter of the year, and 43.3 percent of this (44.3 percent in 2017) fell to the share of December. In general, the expenditures for December amounted to 13.5 percent of total expenditures (12.1 percent in 2017).[10]

Finally, we would like to note that the analysis of the report on the execution of budget shows that the share of expenditures in total budget expenditures for the last quarter was 27.3 percent in 2017, 31.1 percent in 2018, 31.7 percent in 2019, and 29.4 percent in 2020. 44.3 percent of expenditures fell to the share of December in the last quarter of 2017, 43.3 percent in 2018, 55 percent in 2019, and 54.7 percent in 2020. Thus, 12.1 percent of total expenditures in 2017 were executed in December, 13.4 percent in 2018, 17.4 percent in 2019, and 16.1 percent in 2020. However, the proportional expenditure should be 25 percent for quarters and 8.3 percent for months. Of course, deviations from the average for both quarters and months can be observed; however, especially in 2019 and 2020, the deviations made a bigger difference. In this regard, the Opinion of the Chamber of Accounts states that[11] the execution of expenditures at the end of the year creates conditions for the transfer of budget funds to letters of credit, deposits and assignments, bank accounts. In other words, this explanation is a sign of a high risk of corruption in the increased expenditures in December. In fact, this is also observed in practice. Such that budget executors are interested in maximum expenditures, taking into account that expenditures are not left to the next year and that the savings are included in next year's revenues as a free balance. Those who fail to do so during the year do not spend the funds collected at the end of the year by formalizing them in December but write them off through accounting documents. This creates a risk of corruption in the budget. The General Directorate of the Treasury of the Ministry of Finance, which has to prevent this, has not prevented this trend for years. To do this, cash management must be improved and the responsibility of executors must be increased. It seems that there are possible deals between the executors and the treasury.

Risk 3: Billions of manats of unallocated funds, which are included in the budget in the name of unforeseen one-time expenditures.

A significant part of the unspecified expenditures is one-time expenditures. An analysis of international experience shows that the approach of forecasting unspecified expenditures as a reserve in certain sections of the state budget is also used by other countries. The main goal here is to ensure the timely implementation of socio-economic measures to prevent the impact that may occur during the year. However, despite its significant share in the state budget, among the main concepts used in the Law of the Republic of Azerbaijan on Budget System, there is no description and explanation of one-time funds. At the same time, the legal norms on the use of one-time funds are not established in the legislation. This is stated only in Article 19.6 of the Law of the Republic of Azerbaijan on Budget System[12]. According to this article, in coordination with the relevant executive authority (Ministry of Finance), in the process of state budget execution, the savings generated during the reporting year on the one-time funds provided for in the relevant sections, sub-sections, paragraphs, articles, and sub-articles of the economic classification may be directed to the state budget reserve fund and used to finance other measures during the year. By the Law[13] on Amendments to the Law of the Republic of Azerbaijan on Budget System dated December 30, 2016, disposal of one-time funds is limited to the reporting year.

In the budget of 2020, 4,858.7 million manats out of 4,968.1 million manats determined as one-time expenditures were executed, which was at the level of 97.8% of the established purpose. In 2020, 257.0 million manats of these funds were directed to the Reserve Fund of the State Budget as savings for one-time expenditures.[14] For comparison, it should be noted that during the changes made in 2019, a total of 371.3 million manats of savings on one-time expenditures were directed to the Reserve Fund of the State Budget.[15]

As can be seen, last year, as in the previous year, part of the budget expenditures was determined without allocation, even in 2020, the share of unforeseen and unallocated one-time expenditures in the state budget increased compared to the previous year; at the same time, due to the lack of restrictions and regulations on its use, these funds have been spent in irrelevant areas.

It is clear from the report on the budget execution of recent years that one-time funds have been spent without reporting and justification in areas that do not belong to the purpose of the functional unit and do not correspond to its name.

As noted in previous opinions[16] of the Chamber of Accounts, the excess of expenditures, of which allocation is carried out during the year, can also lead to uncertainties about transparency and accountability in the process of execution of public funds by raising questions about the adequacy of budget planning.

According to the information provided on the state budget execution for 2020, the share of the health sector in the functional classification of unallocated (one-time) expenditures was 84.2 percent, the share of the defense and national security sector was 42.7 percent, and the share of services not related to the main sections was 42.2 percent.

Although the obligations created by the COVID-19 pandemic, as well as the 44-day war for the liberation of Karabakh last year, to the state budget led to fundamental changes in the health, defense, and national security sectors, the allocation of 4.5 million manats from the one-time funds by the State Agency of Azerbaijan Automobile Roads for the maintenance of the newly built Central Park in Yasamal district of Baku, the allocation of 1.0 million manats for financial support for the activities of the Caucasian Muslims Office, and the allocation of 6.0 million manats for the purchase of carpets by the Ministry of Culture in the direction of one-time expenditures entitled "Reform costs" raise questions.

Furthermore, the allocation of more than 5 billion manats to public legal entities from various areas of the state budget for 2020 and the financing of these funds from pre-determined expenditures, state capital investment, one-time and event expenditures, expenditures on Reserve Funds raise suspicions of corruption.

Risk 4: The executive makes fundamental amendments in the budget execution process without the consent of parliament.

The Opinion of the Chamber of Accounts on the Execution of the State Budget for 2020[17] states that as in previous years, the amendments made by the relevant executive authorities in the state budget execution process based on some articles of the Law of the Republic of Azerbaijan on Budget System[18] in 2020 had a significant impact on changes in the amounts of the state budget established by the relevant Law and Decree, and, in general, on the state of execution. It should be noted that the amendments made by the relevant executive authorities in the state budget execution process are carried out on the basis of Articles 18.4[19], 18.5[20], and 19.6[21] of the Law of the Republic of Azerbaijan on Budget System. The amendments made in the state budget execution process for 2020 based on these articles, as well as deviations from the scope of application of these articles in 2020 also had a significant impact on the changes in the approved amounts of the state budget and, in general, the state of execution. Although the parliament reconsidered the budget to formalize the deviations until August last year with the amendments made to the budget on the 7th of that month, serious deviations were observed in the budget adopted by the Milli Majlis ordering the final destination of expenditures. I would like to draw your attention to some of them.

Although Article 19.6 of the Law on Budget System allows for directing the savings on one-time expenditures to the State Budget Reserve Fund, there are deviations from this article of the Law. Such that although the amount provided for the State Budget Reserve Fund in 2020 was increased by 439.6 million AZN, of which 257.0 million AZN were one-time expenditures. The remaining 182.6 million AZN were directed to the State Budget Reserve Fund in other areas not provided by Law, in other words, not specified in the Law of the Republic of Azerbaijan on Budget System (non-one-time expenditures).

Furthermore, during the revision of the state budget on August 8, 2020, the amounts of 9 sections on the functional classification of expenditures were reduced by 428.3 million AZN, and the amounts of 3 sections increased by 1,025.8 million AZN. However, despite the increase in costs during the revision of the “Economic activity” section, the costs incurred were less than the original amount.

As can be seen, during 2020, amendments[22] were made in the state budget expenditures both during the revision and in the execution process. These amendments were made by the Ministry of Finance. Referring to Articles 18.4 and 18.5 of the Law of the Republic of Azerbaijan on Budget System, the Ministry of Finance made amendments within sections of functional classification, in sections, auxiliary sections, paragraphs, articles, and sub-articles of economic classification, as well as reduced expenditures on functional, economic (excluding protected expenditure items), and administrative classifications.

The Opinion of the Chamber of Accounts states that the Chamber of Accounts has not received information on the legal basis for amendments made in the budget execution process in 2020. The analysis of the amendments made by the relevant executive authority in the state budget execution process in the reporting year gives grounds to say that these works do not comply with the Law of the Republic of Azerbaijan on Budget System.

Hence, the Opinion of the Chamber of Accounts states that although Article 18.4 of the Law on Budget System allows for amendments only in the functional classification within the section, the amendments made in the budget execution process in 2020 also included amendments outside the section. Moreover, despite the fact that the Ministry of Finance has the right to make amendments according to Article 18.5 of the Law if the funds provided for the financing of revenues and deficits are less than the approved amount, the Ministry of Finance sent information to budget organizations and organizations receiving financial assistance from the budget on the reduction of their respective budgets in April; however, by the end of that month, the forecasts for both revenues and deficit financing sources were exceeded.

In fact, all this gives grounds to say that by making unlimited changes compared to the initially approved indicators, the Ministry of Finance has misappropriated the powers of the Milli Majlis in the execution process of the 2020 state budget and created risks for corruption.

It is true that this is justified by Articles 18.4, 18.5, and 19.6 of the Law of the Republic of Azerbaijan on Budget System in many cases but there are also deviations from the Law.

Even the Ministry of Finance has the potential to improve on each of the three articles (Articles 18.4, 18.5, and 19.6) of the Law of the Republic of Azerbaijan on Budget System referred to when making fundamental amendments. Such that the words "if necessary" used in Article 18.4 of the Law should be replaced by the numerical restrictions applied in the practice of other countries (Georgia, Kazakhstan, Kyrgyzstan, Ukraine, Uzbekistan). At the same time, any amendments made within the section (for example, transfers from capital expenditures to current expenditures) should be restricted.

Significance of the share of one-time expenditures in the state budget for 2020, use of these expenditures in areas not related to the purpose of the functional unit and not in accordance with its name, directing expenditures in predictable directions, lack of limits for forecasting funds in these areas have a negative impact on both the reliability and relevance of the budget. Therefore, Article 19.6 of the Law should clarify the concept of one-time expenditures in the legislation.

Finally, Article 18.5 of the Law does not define legal norms related to numerical restrictions. However, in the advanced world practice, a number of countries have set limits in this direction, and it was determined to what extent the limits were decided by the executive authorities and the Parliament. Azerbaijan should also use this practice and limit the exclusive right of the executive branch in this process by regulating its powers for amendments in the budget execution process.

Risk 5: Balances (debts) on revenues provided to the state budget are increasing.

In the reports on budget revenues provided by the tax authorities (mainly by the end of 2020), the amount of balances (debts) to the state budget increased by 334,441.4 thousand manats or 27.7 percent compared to the beginning of the year and amounted to 1,541,252.4 thousand manats, the main amount of tax increased by 201,302.9 thousand manats or 24.4 percent and amounted to 1,025,581.3 thousand manats, the amount of financial sanctions increased by 64,021.9 thousand manats or 40.5 percent and amounted to 222,009.0 thousand manats, and the amount of interest increased by 69,116.6 thousand manats or 30.8 percent and amounted to 293,662.1 thousand manats.

As can be seen, although the amount of balances (debts) to the state budget has increased, it is not classified by sectors and companies. This is explained by the fact that according to the Law of the Republic of Azerbaijan on Commercial Secrets[23], tax payments of companies are considered information that is considered a commercial secret. In fact, information on the amount of balances (debts) to the state budget by the end of the year for taxpayers should be disclosed and transparency should be ensured in order to reduce the corruption risks in such cases.

Risk 6: The management of the balance of the single treasury account is not transparent and accountable.

Despite the reduction of the balance of the single treasury account in 2020 in the equivalent of 816.1 million manats, its amount at the end of the reporting year amounted to 1,526.1 million manats. $ 377.0 million of the free balance of the single treasury account was transferred to the management of the State Oil Fund, 8.4 million manats were deposited in Azer-Turk Bank for 5 years, and the remaining funds were placed in the bank accounts of the treasury. Apparently, a large part of the funds was left out of management, and access to information on the amounts placed in the bank accounts of the treasury was not provided. On the other hand, the management of the State Oil Fund does not provide information on the income received from the deposits of Azer-Turk Bank, which may create conditions for corruption risks in the management of the balance of the single treasury account.

In conclusion, I would like to note that the analysis of data on the state budget execution for 2020 shows that the central executive authorities have been able to take advantage of the existing legal gaps in the budget in the execution process. They did all this in violation of the requirements of transparency and accountability, without taking into account the comments and suggestions of the Chamber of Accounts in previous years, which were repeated in 2020. This has further increased the corruption risks in the budget execution process.

Gubad Ibadoglu

[1] On the Execution of the State Budget of the Republic of Azerbaijan for 2020, http://maliyye.gov.az/scripts/pdfjs/web/viewer.html?file=/uploads/news_files/60bf5fea2c234.pdf

[2] Opinion of the Chamber of Accounts on the Annual Report on the Execution of the State Budget for 2020, https://sai.gov.az/files/2020-%C4%B0cra-R%C9%99y%20(3)-188749903.pdf

[3] On Amendments made to the Decree of the President of the Republic of Azerbaijan No. 668 dated January 29, 2002, on the Application of the Law of the Republic of Azerbaijan on Amendments to the Law of the Republic of Azerbaijan on Public Procurement No. 1433-VQD dated December 28, 2018, and on the Application of the Law of the Republic of Azerbaijan on Public Procurement, http://e-qanun.az/framework/41180

[4] Decree of the President of the Republic of Azerbaijan on the Application of the Law of the Republic of Azerbaijan on Public Procurement, http://www.e-qanun.az/framework/1079

[5] http://www.consumer.gov.az/

[6] Law of the Republic of Azerbaijan on Public Procurement, http://www.e-qanun.az/framework/1029

[7] Decree of the President of the Republic of Azerbaijan No. 668 of January 29, 2002, on the Application of the Law of the Republic of Azerbaijan on Public Procurement, http://www.e-qanun.az/framework/1079

[8] Increasing transparency in public procurement, http://kafondu.org/wp-content/uploads/2020/08/Satinalamalar_Hesabat_T%C4%B0_Azerbaijan_New.pdf

[9] Opinion of the Chamber of Accounts of the Republic of Azerbaijan on the Draft Law of the Republic of Azerbaijan on the Execution of the State Budget of the Republic of Azerbaijan for 2019 and the Annual Report on the Execution of the State Budget, https://sai.gov.az/files/2019-REY_%C4%B0CRA.pdf

[10] Opinion of the Chamber of Accounts of the Republic of Azerbaijan on the Draft Law of the Republic of Azerbaijan on the Execution of the State Budget of the Republic of Azerbaijan for 2018 and the Annual Report on the Execution of the State Budget, https://sai.gov.az/files/ICRA-2018-FINAL(1).pdf

[11] Opinion of the Chamber of Accounts on the Annual Report on the Execution of the State Budget for 2020, https://sai.gov.az/files/2020-%C4%B0cra-R%C9%99y%20(3)-188749903.pdf

[12] Law of the Republic of Azerbaijan on Budget System, http://www.e-qanun.az/framework/1126

[13] Law on Amendments to the Law of the Republic of Azerbaijan on Budget System, http://e-qanun.az/framework/34618

[14] Opinion of the Chamber of Accounts on the Draft Law of the Republic of Azerbaijan on the Execution of the State Budget of the Republic of Azerbaijan for 2020 and the Annual Report on the Execution of the State Budget for 2020, https://sai.gov.az/files/2020-%C4%B0cra-R%C9%99y%20(3)-188749903.pdf

[15] Opinion of the Chamber of Accounts on the Draft Law of the Republic of Azerbaijan on the Execution of the State Budget of the Republic of Azerbaijan for 2019 and the Annual Report on the Execution of the State Budget, https://sai.gov.az/files/2019-REY_%C4%B0CRA.pdf

[16] Opinions of the Chamber of Accounts, https://sai.gov.az/filter?type=rey

[17]Opinion of the Chamber of Accounts on the Annual Report on the Execution of the State Budget for 2020, https://sai.gov.az/files/2020-%C4%B0cra-R%C9%99y%20(3)-188749903.pdf

[18]Law of the Republic of Azerbaijan on Budget System, http://www.e-qanun.az/framework/1126

[19]If necessary, within the limits of the approved budget allocations, changes may be made by the relevant executive authority within the sections of the functional classification, in sections, auxiliary sections, paragraphs, articles, and sub-articles of the economic classification.

[20]In the state budget execution process, when revenues and funds intended for financing the deficit are received less than the approved amount, expenditures on functional and economic classification (excluding protected expenditure items) may be reduced proportionally, and expenditures on administrative classification may be reduced in accordance with the procedure established by the relevant executive authority.

[21] In coordination with the relevant executive authority, the savings generated during the reporting year on one-time funds provided for in the relevant sections, auxiliary sections, paragraphs, articles, and sub-articles of the economic classification in the state budget execution process may be directed to the state budget reserve fund and used to finance other activities during the year.

[22] Law of the Republic of Azerbaijan on Amendments to the Law of the Republic of Azerbaijan on the State Budget of the Republic of Azerbaijan for 2020, http://e-qanun.az/framework/45672

[23]Law of the Republic of Azerbaijan on Commercial Secrets, http://www.e-qanun.az/framework/2861

Analytics

-

In a significant diplomatic move, President Kassym-Jomart Tokayev of Kazakhstan embarked on an official visit to Armenia, marking a pivotal moment in the relationship between the two nations. The meeting between President Tokayev and Armenian Prime Minister Nikol Pashinyan resulted in the signing of a joint statement aimed at fostering cooperation and easing tensions that had simmered between the two countries.

Leave a review